Entrepreneurs are hungry. But it's not just because they're living on ramen and adrenaline while they pour their all into their business. Peter Cohan has found it's something deeper: a hunger to create the kind of world they want to work in.

The first research-based book on business strategy for start-ups

Based on Cohan's venture investment experience and on his interviews with over 150 start-up CEOs

Offers specific approaches for six critical start-up decisions

Entrepreneurs are hungry. But it's not just because they're living on ramen and adrenaline while they pour their all into their business. Peter Cohan has found it's something deeper: a hunger to create the kind of world they want to work in. To leave a legacy, they build carefully with limited resources and maintain control of the venture's direction.

For years, students have told Cohan that the seminal business strategy guide, Michael Porter's Competitive Strategy, was too big-company focused. So Cohan -- who once worked with Porter-has written the first business strategy book to address start-ups' very different challenges.

Cohan focuses on six key start-up choices-setting goals, picking markets, raising capital, building teams, gaining market share, and adapting to change-explaining the unique rules start-ups must follow. For example, when setting goals, large corporations try to maximize their long-term return on equity, but resource-poor start-ups have to plan by setting a series of short-term goals-and how they do this will mean the difference between blazing a trail or flaming out. When entering a new market, well-fed companies can invest substantial time and capital before ever launching a product, but hungry start-ups must get an adequate prototype in front of customers fast, get feedback, and quickly develop a viable business model or they'll starve to death.

For each of these six areas, Cohan provides a decision-making approach and lively case studies of what actual entrepreneurs have done. He extracts hard-hitting lessons not only for start-ups but also for investors and even established companies. Hungry Start-up Strategy offers a full menu of vital information for anyone seeking to cook up a thriving business from scratch.

The first research-based book on business strategy for start-ups

Based on Cohan's venture investment experience and on his interviews with over 150 start-up CEOs

Offers specific approaches for six critical start-up decisions

Entrepreneurs are hungry. But it's not just because they're living on ramen and adrenaline while they pour their all into their business. Peter Cohan has found it's something deeper: a hunger to create the kind of world they want to work in. To leave a legacy, they build carefully with limited resources and maintain control of the venture's direction.

For years, students have told Cohan that the seminal business strategy guide, Michael Porter's Competitive Strategy, was too big-company focused. So Cohan -- who once worked with Porterhas written the first business strategy book to address start-ups' very different challenges.

Cohan focuses on six key start-up choicessetting goals, picking markets, raising capital, building teams, gaining market share, and adapting to changeexplaining the unique rules start-ups must follow. For example, when setting goals, large corporations try to maximize their long-term return on equity, but resource-poor start-ups have to plan by setting a series of short-term goalsand how they do this will mean the difference between blazing a trail or flaming out. When entering a new market, well-fed companies can invest substantial time and capital before ever launching a product, but hungry start-ups must get an adequate prototype in front of customers fast, get feedback, and quickly develop a viable business model or they'll starve to death.

For each of these six areas, Cohan provides a decision-making approach and lively case studies of what actual entrepreneurs have done. He extracts hard-hitting lessons not only for start-ups but also for investors and even established companies. Hungry Start-up Strategy offers a full menu of vital information for anyone seeking to cook up a thriving business from scratch.

Orders of 10+ copies shipping to one address receive free ground shipping

within the U.S. Shipping to separate individual addresses via USPS media mail will be applied a handling fee:

Book Details

Overview

Entrepreneurs are hungry. But it's not just because they're living on ramen and adrenaline while they pour their all into their business. Peter Cohan has found it's something deeper: a hunger to create the kind of world they want to work in.

The first research-based book on business strategy for start-ups

Based on Cohan's venture investment experience and on his interviews with over 150 start-up CEOs

Offers specific approaches for six critical start-up decisions

Entrepreneurs are hungry. But it's not just because they're living on ramen and adrenaline while they pour their all into their business. Peter Cohan has found it's something deeper: a hunger to create the kind of world they want to work in. To leave a legacy, they build carefully with limited resources and maintain control of the venture's direction.

For years, students have told Cohan that the seminal business strategy guide, Michael Porter's Competitive Strategy, was too big-company focused. So Cohan -- who once worked with Porter-has written the first business strategy book to address start-ups' very different challenges.

Cohan focuses on six key start-up choices-setting goals, picking markets, raising capital, building teams, gaining market share, and adapting to change-explaining the unique rules start-ups must follow. For example, when setting goals, large corporations try to maximize their long-term return on equity, but resource-poor start-ups have to plan by setting a series of short-term goals-and how they do this will mean the difference between blazing a trail or flaming out. When entering a new market, well-fed companies can invest substantial time and capital before ever launching a product, but hungry start-ups must get an adequate prototype in front of customers fast, get feedback, and quickly develop a viable business model or they'll starve to death.

For each of these six areas, Cohan provides a decision-making approach and lively case studies of what actual entrepreneurs have done. He extracts hard-hitting lessons not only for start-ups but also for investors and even established companies. Hungry Start-up Strategy offers a full menu of vital information for anyone seeking to cook up a thriving business from scratch.

The first research-based book on business strategy for start-ups

Based on Cohan's venture investment experience and on his interviews with over 150 start-up CEOs

Offers specific approaches for six critical start-up decisions

Entrepreneurs are hungry. But it's not just because they're living on ramen and adrenaline while they pour their all into their business. Peter Cohan has found it's something deeper: a hunger to create the kind of world they want to work in. To leave a legacy, they build carefully with limited resources and maintain control of the venture's direction.

For years, students have told Cohan that the seminal business strategy guide, Michael Porter's Competitive Strategy, was too big-company focused. So Cohan -- who once worked with Porterhas written the first business strategy book to address start-ups' very different challenges.

Cohan focuses on six key start-up choicessetting goals, picking markets, raising capital, building teams, gaining market share, and adapting to changeexplaining the unique rules start-ups must follow. For example, when setting goals, large corporations try to maximize their long-term return on equity, but resource-poor start-ups have to plan by setting a series of short-term goalsand how they do this will mean the difference between blazing a trail or flaming out. When entering a new market, well-fed companies can invest substantial time and capital before ever launching a product, but hungry start-ups must get an adequate prototype in front of customers fast, get feedback, and quickly develop a viable business model or they'll starve to death.

For each of these six areas, Cohan provides a decision-making approach and lively case studies of what actual entrepreneurs have done. He extracts hard-hitting lessons not only for start-ups but also for investors and even established companies. Hungry Start-up Strategy offers a full menu of vital information for anyone seeking to cook up a thriving business from scratch.

About the Author

Peter Cohan (Author)

Peter S. Cohan is a management consultant, venture capitalist, teacher, author and blogger. Prior to starting his management consulting and venture capital firm in 1994, he worked for Monitor Company, a strategy consulting firm co-founded by HBS Professor, Michael Porter and as an internal consultant in the banking and insurance industries. His firm has completed over 150 consulting projects for companies and govenments. He has invested in six private companies, three of which were sold for a total of $2 billion. He teaches business strategy to undergraduate and MBA students at Babson College; has authored 11 books; and writes the ""Startup Economy"" column for Forbes and the ""Hungry Start-up"" column for Inc. He earned an MBA from Wharton, did graduate work in Computer Science at MIT, and holds a BS in Electrical Engineering from Swarthmore College.

Table of Contents

Preface

Introduction

PART ONE

SIX START-UP CHOICES

1 Setting Goals: What Makes You Hungry?

2 Picking Markets: Feed Your Customers and They'll Feed You

3 Raising Capital: Maintain Your Fighting Weight

4 Building the Team: Whom Do You Invite to the Table?

5 Gaining Share: Satisfy Your Customers' Cravings

6 Adapting to Change: Don't Let Others Eat Your Lunch

PART TWO

IMPLICATIONS FOR STAKEHOLDERS

7 Straight Talk from Start-Up Capital Providers

8 Can Big Companies Train Entrepreneurs?

9 Resources

Notes

Acknowledgments

Index

About the Author

Preface

Introduction

PART ONE

SIX START-UP CHOICES

1 Setting Goals: What Makes You Hungry?

2 Picking Markets: Feed Your Customers and They'll Feed You

3 Raising Capital: Maintain Your Fighting Weight

4 Building the Team: Whom Do You Invite to the Table?

5 Gaining Share: Satisfy Your Customers' Cravings

6 Adapting to Change: Don't Let Others Eat Your Lunch

PART TWO

IMPLICATIONS FOR STAKEHOLDERS

7 Straight Talk from Start-Up Capital Providers

8 Can Big Companies Train Entrepreneurs?

9 Resources

Notes

Acknowledgments

Index

About the Author

Excerpt

Hungry Start-up Strategy

CHAPTER 1

Setting Goals What Makes You Hungry?

START-UPS ARE BORN HUNGRY—their demand for money exceeds their supply. So start-ups need a different currency—a powerful emotional magnet that draws in talent.

Why would anyone go to work for a start-up? The hours are sure to be longer than they would be at a more established company, and the pay is likely to be lower as cash will be in short supply.

The simple answer is that some talented people are able to defer short-term economic gain in exchange for meaningful work with the possibility of a longer-term payoff.

Of course, this puts entrepreneurs in the difficult position of persuading talented people that they should stop whatever they are doing and work for them instead. And as we’ll see in Chapter 3, entrepreneurs must also persuade capital providers to part with their cash to invest in their start-ups.

To recruit talented employees, entrepreneurs must mint emotional currency by way of three hungry start-up goals. These three goals answer the basic questions a talented potential employee might have before going to work for your start-up.

Why should I join your start-up?Mission. The mission is the entrepreneur’s most compelling case for why the start-up is going to achieve greatness. At the core of this case is a passionately held belief that what the start-up aspires to do is important. As we’ll see, that passion might come from the desire to make the world a better place, the excitement that comes from being certain that the start-up could capture a great economic opportunity that nobody else has seen, or the simple desire to solve a problem that perplexes the founder.

How will I get a return on the stock I receive in exchange for giving up my life to your start-up over the next five years?Long-term goals. Long-term goals describe a tangible way that the entrepreneur will measure the venture’s success, say, five years into the future. Long-term goals include being the leader in an important new market, becoming a big public company, being acquired by a bigger company, or remaining permanently private and independent.

How will you actually deliver on that promise?Short-term goals as a series of real options. Short-term goals are specific milestones that the entrepreneur sets over a period of months, and the idea of real options means that each short-term goal is a frugal experiment. Setting good short-term goals reflects how effective the CEO is at getting stuff done. Many of the start-ups I interviewed tend to view these short-term goals as a sequence of go/no-go decisions. For example, the first short-term goal might be to figure out the start-up’s business model, the next might be to get customers to use or pay for the product, and the third to expand success from one market to five around the world. If the entrepreneur can figure out, say, the first goal—e.g., the start-up’s business model—then she continues on to the second one. Otherwise, she shutters the venture.

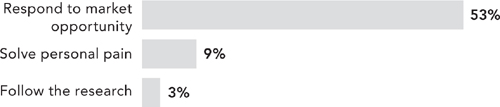

MISSION: RESPOND TO MARKET OPPORTUNITY, SOLVE PERSONAL PAIN, AND FOLLOW THE RESEARCH

As Figure 1.1 illustrates, entrepreneurs have different ways of picking a start-up’s mission.

Entrepreneurs get the ideas to start companies from three sources:

In many cases, it appeared clear that the founders did not consider their emotional or intellectual connection to the start-up to be a sufficiently compelling reason to devote themselves to a company. Instead, they felt a need to go beyond that personal impulse and determine whether there was a big enough market opportunity to justify the investment of time and money in starting the venture.

FIGURE 1.1 Why Entrepreneurs Start Companies, by Percent of Interviewees.

This is not to say that the ventures that were started purely to relieve personal pain or develop an intellectual interest did not eventually coincide with a market opportunity. Rather, these entrepreneurs were willing to defer identifying that opportunity at the time they started the company. Of the start-ups I interviewed, 24 percent sprang from a combination of personal pain and perceived market opportunity, and 10 percent were born of a combination of or intellectual interest and perceived market opportunity.

Let’s take a look now at examples of each kind of mission.

Respond to Market Opportunity

Responding to market opportunity is the most common reason that entrepreneurs start companies. Their mission is to satisfy that unmet need better than the competition and build a significant enterprise in the process.

The specific nature of the market opportunity varies for each start-up and some are more studious than others when it comes to talking with customers to get external evidence to support their belief that the market opportunity is real.

Among the start-ups I interviewed were for-profits and social enterprises. And one interesting feature of these examples is that two of them—SoFi and m-Via—combine pursuit of market opportunity with a bigger social purpose. Here are some examples of the market opportunities that the for-profit start-ups perceived:

I saw an opportunity in the $1 trillion student loan market to lower the rates that students pay on their loans while creating an attractive investment opportunity for alumni.33

— Mike Cagney, co-founder and CEO of SoFi, and former vice president and head trader of Wells Fargo. SoFi raises capital from alumni at colleges to help finance loans to their students.

ExtraHop was founded in early 2007; my co-founder and I saw an underserved market. We are targeting a large, fast-growing market. After all, Gartner estimated that the market for network and application performance monitoring products hit $3.8 billion in 2011 and is growing at an 8.5 percent annually. And we were eager to solve the problem. We spent over two years working on building a product that would work well for the customers with whom we collaborated.34

— Jesse Rothstein, CEO of Extrahop, a sub-$50,000 appliance that provides IT managers with real-time system health and performance information.

I see a big opportunity in a very fast-growing industry. IDC reports that between 2001 and 2011, the market for our product—virtualization storage—grew from scratch to $11 billion. Before founding Tintri, I oversaw the development of all server virtualization technology for VMware as its VP of R&D from 1999 to 2006. I recognized the problem server virtualization created for storage early on and resolved to shift my career focus to solve this storage dilemma. To that end, I founded Tintri—it’s Gaelic for “lightning.” My aim was to extend the benefits of virtualization from the server side to storage—what could be a lightning bolt of efficiency if carried out.35

— Kieran Harty, CEO of Tintri, which helps companies store and retrieve information more efficiently.

While working at a mobile gaming start-up, I grew increasingly outraged as I analyzed the way the cross-border money transfer business has skillfully avoided disruption of its tactics over the last thirty years. I felt that it was unfair to exploit the weakness of people sending money home and became convinced that I could develop a service that would offer them a lower-cost, safer way to transfer money.36

— Bill Barhydt, CEO of m-Via, which helps people wire money to their families in Mexico and other countries.

From these examples, the takeaway is simple. Start-up CEOs should set their start-up’s mission based on their own experience. But the mission should be bolstered by some external validation: ideally, in-depth customer research that confirms that what is important to the founder will also be important to a sizable audience.

This same principle holds for social enterprises—set up not for profit, but to make the world better. What’s different about them is that they face a unique challenge in their efforts to achieve what is most commonly a very noble social purpose. It’s challenging for social enterprises to make enough money to perpetuate doing social good. Here are some examples:

One of the reasons I started PoverUP was that in the summer of 2008, I volunteered in a border refugee village in Thailand. That’s where I realized that a little money—I bought 50 donuts for $1—could go a long way to helping poor people start businesses that would lift them out of poverty.37

— Charlie Javice, co-founder and CEO of PoverUP, a social network for university students to get involved in social enterprises.

I developed the idea for a peer-to-peer donation service in 2005 while pursuing my master’s degree in Industrial Engineering at Stanford after visiting Indonesia a few months before the December 2004 tsunami struck. Following the relief efforts, I saw stockpiles of usable medicine, large enough to overflow a football stadium, not only not being used but also costing Indonesia millions of dollars to dispose of as toxic waste. I started SIRUM to solve the supply chain problem that prevented perfectly good medicine from getting to the people who needed it.38

— Adam Kircher, founder of SIRUM, a nonprofit that gets medication that would otherwise be dumped or incinerated into the hands of poor people in California.

A mother living in a rural village outside of Bangalore, India, gives birth to a baby two months prematurely. Her family cannot afford to go to the city hospital in Bangalore, so her husband, who raises silkworms that he warms under lamps, decides to care for the baby in the same way. A few days later, their insufficiently warmed baby dies. Stopping this tragedy—20 million low-birth-weight and premature babies are born each year—is the primary mission of Embrace.39

— Jane Chen, founder and CEO of Embrace, which makes a sleeping-bag–like baby warmer that helps improve the odds of survival for premature babies born in developing countries.

Lacking the potential to attract people motivated by an opportunity to become wealthy, the missions of these social enterprises must be particularly compelling. And these examples do share the following common characteristics:

They all spring from emotionally powerful and compelling stories about why the organization was formed.

They attract talented people who want to help achieve that long-term goal.

It is clear who will benefit from achieving the goal.

The founders are likely to face a challenge as they attempt to maintain unswerving devotion to their long-term goals and generating sufficient cash flow to keep their organizations operating.

Solve Personal Pain

While the majority of start-ups I interviewed set their long-term goals based on a perceived market opportunity, some believed so strongly in the importance of addressing their personal pain that they went ahead with their companies without hard evidence of a significant market opportunity.

Here are some examples of the personal pain that spurred the creation of for-profit start-ups:

I got the idea for AfterSteps after a grandparent died. My mother started calling me in periodic spurts with her estate plans, wishes for various personal items, and requests for how to handle her body. I decided there had to be a better way. So I started AfterSteps to bring organization, completeness, and knowledge to the end-of-life planning process.40

— Jesse Bloomgarden, founder and CEO of AfterSteps, a service that helps people prepare their loved ones for their death.

Before starting Huddle, I worked for a “big data” firm called Dunn-humby—it analyzed data for large retailers such as Procter & Gamble—where I led a business that grew to $60 million in revenues in three years. When the company was acquired, I left. I used some of the proceeds from the sale to finance Huddle’s initial operations in 2008. I wanted to solve a problem I had at Dunnhumby—my 300-person staff could not work together on projects through a single, easy-to-use system. Huddle was started to remedy that problem.41

— Alastair Mitchell, founder and CEO of Huddle, a service that enables big companies collaborate on projects.

I attended an all-girls high school in India and was then admitted to one of its top engineering programs, IIT Kanpur, India. There, I was one of three girls in a class of fifty computer science majors. I was shy and studied alone while the more gregarious boys collaborated. As a result, the boys, working together, could get answers in ten minutes to questions that I spent four hours solving myself. Piazza is my way of letting the shy and the gregarious of both sexes collaborate online. I believe that Piazza works better than wikis and threaded discussion groups that are often used for student Q&A.42

— Pooja Nath Sankar, CEO of Piazza, a service that helps students ask questions of peers and professors and get the best answers at the top.

These stories all share certain common characteristics that typify entrepreneurs seeking to solve personal pain:

The start-up CEOs each had a compelling personal problem and wanted to develop a business dedicated to solving that problem.

The CEOs were willing to invest their time and money in developing a solution to their problems and did not let the absence of a clear market opportunity stop them.

The CEOs assumed that if they could solve the problem well, they would find plenty of other people who would pay them for the solution.

While the long-term success cannot yet be predicted for any of these ventures, their goals serve a useful purpose. By choosing long-term goals that relieve their pain, there is little doubt that these founders will have ample motivation to solve the problem effectively.

And in these cases, it does not take a precise market size estimate for the founders to apply some common sense and realize that their pain is widely shared—even if the precise size of the market is not of great interest to them in setting long-term goals for their companies.

Follow the Research

A few of the start-ups I interviewed were started by people with PhDs who decided to try to turn their doctoral research into a business. While this is a fairly risky business proposition, there is often a chance that their original research can be applied to an existing problem for which there is not a particularly good solution. It is also possible that their work can create a market where one has not previously existed.

Here are some examples of how following the research spurred the creation of two start-ups:

Sifteo CEO Jeevan Kalanithi, a colleague from Stanford, and I were studying at MIT’s Media Lab. He shared my interest in bringing physical objects such as dominoes back to interactive gaming. We wondered together why everything on our computers—email, files, and icons—were two-dimensional. We wanted to bring three-dimensionality to computing—to develop siftable computers that people could use their hands to manipulate—to sift and sort—like a pile of LEGOs. In the summer of 2009, we founded Sifteo to build products that would fulfill our vision for hands-on interaction.43

— Dave Merrill, co-founder and president, Sifteo, which makes blocks with programmable screens that can interact wirelessly.

I took a leave of absence from my Stanford master’s degree program in computer science after earning a BS in the field—I have four classes left—to start Loki Studios. At Stanford, I met an engineer who shared my passion for the idea of starting a gaming company that would take advantage of mobile technologies.44

— Ivan Lee, CEO of Loki Studios, a maker of mobile Pokemon-like games.

It’s not very often that entrepreneurs start companies to follow the research; however, they:

Each had a strong interest in applying new technologies to games.

All came up with novel ways to apply existing technologies to their interest in games.

Assumed that if they could solve the problem well, they would be able to create a market of people who would be willing to pay for their solution.

While these intellectual ventures both got started without substantial research into the market potential for the products that they were developing, it is clear from talking with the founders that they would be happy to develop their products and get them working well. If they happened to find sizable numbers of other people who shared their interest, they would be delighted.

So, if you are an entrepreneur who wants to follow the research, you should consider raising capital from investors who share your interest in the field.

Solve Personal Pain and Respond to Market Opportunity

As noted previously, about a quarter of the companies I interviewed started companies to relieve personal pain and because they believed that there would be a big market opportunity in so doing.

Here are some examples:

I left my driveway at 9 a.m. for a doctor’s appointment; I signed in, waited a few hours, and finally got in to see my doctor, who prescribed medication. I get back in the car, drove to the pharmacy, waited in a line for my prescription, and paid for it. By the time I returned to the driveway, it was 2:30 in the afternoon. A fine day, wasted. I was thinking about starting a new company targeting a big market and when I was returning from the pharmacy that day, I realized that health care would fit the bill. So I decided to start WhiteGlove Health.45

— Bob Fabbio, CEO of WhiteGlove Health, which provides health care to corporate employees in their homes or offices.

I like to take photographs. In 2003, I had what I thought was a great collection that I wanted to use for a book to give 35 friends and family members. One little problem—the price tag for doing that would be a jaw-dropping $10,000. I thought that given the technology available at the time, it should not be so hard to produce that book. I set up Blurb to solve that problem. I immediately set out to research whether there would be a big enough market to make a start-up worthwhile and discovered that the opportunity was worth pursuing.”46

— Eileen Gittins, founder and CEO of Blurb, a service that lets people self-publish, with an emphasis on books with digital images.

I bought some security cameras to protect my business and noticed that their quality was terrible. Having expertise in high-quality camera hardware and software, I started a company focused on building much better surveillance systems. We’re targeting the $10 billion market for surveillance systems—half of which is cameras and the other half video management software. The market is growing between 5 and 15 percent a year, and we are tapping the fastest-growing upgrade segment.47

— Alexander Fernandes, CEO of Avigilon, which makes inexpensive, high-quality visual surveillance systems.

These stories share certain common characteristics that typify entrepreneurs seeking to solve personal pain and respond to market opportunity:

The start-up CEOs each had a compelling personal problem and wanted to develop a business dedicated to solving that problem.

They were not willing to bet their time and money on the opportunity unless they could be convinced that there would be enough other people who had the same problem and would be willing to pay to solve it.

Their research gave them confidence that the market opportunity for solving that problem would more than offset the likely investment required to develop a solution and sell it to those potential customers.

This combination of reasons for setting a start-up’s long-term goal is among the most compelling ones out there. The existence of a personal problem that the founder wants to solve is a powerful spur to invest time and money in solving it. And the ability to gather compelling evidence that the number of potential customers is big enough to justify that investment is likely to interest potential employees and investors.

Follow the Research and Respond to Market Opportunity

Some of the start-ups I interviewed combined their desire to follow the research with what I think is a sensible urge to find whether the demand for their product will justify the investment of their time and money.

Here are some examples of companies that followed the research and responded to a market opportunity:

Company co-founder Marsha Moses and the late Judah Folkman of Boston’s Children’s Hospital invented a urine-based, noninvasive cancer detection technology that Predictive Biosciences has commercialized. Monitoring bladder cancer patients after their initial treatment is very expensive. Patients must submit to cystoscopy—threading a cystoscope through their urethra and into the bladder—every three months for the first two years, every six months for the next two years, and annually thereafter. Replacing this invasive test with one that detects biomarkers in the urine targets a $3 billion market for bladder cancer detection.48

— Peter Klemm, CEO of Predictive Biosciences, which makes diagnostic tests for diseases like colon and prostate cancer.

I started Locately in 2008 with the idea of applying location analysis to the then recently introduced Apple iPhone. To finance the company, I and fellow MIT PhD, Eric Weiss, saw success in the MIT $100K Entrepreneurship Competition. Our idea was to make use of valuable location data from mobile devices [that were] going unprocessed and unharnessed every single day. And we saw a business opportunity in packaging and analyzing that data for national brands, market researchers, and advertisers. Our goal was to provide new insights into consumers’ location-relevant lifestyles while keeping individuals always in control of their data.49

— Dr. Thaddeus Fulford-Jones, CEO of Locately, a service that helps retailers track consumers’ shopping behavior as their locations change.

These stories share certain common characteristics that typify entrepreneurs seeking to pursue an intellectual interest coupled with a market opportunity:

The start-up CEOs each had invested a significant amount of time developing the intellectual interest, and it took the form of a doctoral thesis or postdoctoral research.

In some cases, the people who conducted the research had no interest in capitalizing on it themselves; however, they did want to license their work to someone with a track record of successfully commercializing such intellectual property.

If the market opportunity for applying the research is sufficiently attractive, the combination of the unique, patented technology with a significant, unmet market need can set the stage for a successful venture with a clear long-term goal that galvanizes executives, capital providers, and workers.

As an investor, I find this combination of intellectual originality and market opportunity to be generally quite compelling. Potential employees would also be likely to find the goal of building such a start-up to be attractive.

There are many kinds of long-term goals that entrepreneurs can set for their start-ups. In general, hungry start-ups set these long-term goals with the idea that they will help shape the work environment that they want to create. So whether the long-term goal springs from personal pain, an intellectual interest, a market opportunity, or a combination of these, the most important thing for the company is that the founders firmly believe in their long-term goals.

Their belief in these long-term goals will motivate them to commit their time and capital, if necessary, to achieve them. That belief will also help them attract employees and capital to help achieve those goals.

THE REAL-OPTIONS APPROACH

Hungry Start-Up Approach to Short-Term Goals: A Series of Real Options

Hungry start-ups are so short on cash that what they choose to do in the short term can make the difference between surviving and running out of money. Rather than betting all their cash on one big goal, start-ups set shorter term goals—such as building a prototype of a product and getting customer feedback on it within six months.

Principles of Hungry Start-Up Approach to Short-Term Goals

Start-up CEOs think of those short-term goals as real options—inexpensive, time-limited bets. And these options will either generate a successful outcome or a failed one from which the start-up can learn and adapt. More formally, start-up CEOs think of short-term goals as a sequence of real options which give their holders the right, but not the obligation, to make future investments in the start-ups.50

Here start-ups conduct a series of frugal experiments51 where they spend a relatively small amount of money to test a hypothesis about a potential opportunity. Through this hypothesis testing, start-ups get insight about the nature of the opportunity, which they can use to decide whether to buy another option—by making a new frugal experiment52—or to stop their experiment.

To set short-term goals through a real-options approach, entrepreneurs should follow three principles:

Use goals to limit risk and encourage learning. The real-options approach to goal setting also forces managers to break up the very daunting challenge of building a company from scratch into more manageable bits. The art of this real-options approach is to sequence the goals so that if the first one is achieved, it will provide learning that helps to achieve the second one. The same logic applies to jumping from the second to the third goal in the sequence. Even if the company fails to achieve all the goals, if managers choose and sequence them properly, investors can limit their risk of loss.

Set goals that are ambitious, yet achievable. One of the primary reasons to set goals is that they help communicate to employees why they are there—and in the case of start-ups, why they are working so many hours. Setting ambitious yet achievable goals can motivate people. With start-ups the term of those goals is measured in months, rather than years. To achieve such short-term goals demands a very high level of concentrated effort. And a larger firm with a slower cycle time may be vulnerable to the efforts of a start-up that targets the larger firm’s customers.

Use goals to map the company’s growth path. Finally, the real-options approach to goal setting can put the company on a steep growth path. For instance, Adeptol, which offers a browser-based document reader, is owned by its founder and CEO, Prateek Kathpal. Adeptol had 2,000 customers when I talked with Kathpal after it had been in business for a mere two years.53 And Apptio—which offers a service that helps companies’ chief technology officers explain the costs and the value of their services to their corporate customers—has also exceeded ambitious short-term goals. For example, CEO Sunny Gupta set a year-two goal of 300 percent growth which Apptio surpassed by a factor of three.54 Apptio’s ability to exceed its goals highlights the motivational power of setting them and the appeal of its service to customers.

Hungry Start-Up Approach to Short-Term Goals: Defined

Goal setting—a firm’s process of deciding what measurable outcomes it wants to achieve—is a critical starting point because it focuses all of its subsequent actions. Simply put, a company’s strategy flows from its goals.

Start-ups’ goals vary. Based on my research, if a company is largely controlled by external venture capitalists, then their goals will prevail. In general, VCs want to make an investment and sell it within a period of years at the highest price that another company or public investors are willing to pay.

Since start-up CEOs generally seek out VCs who share their goals and their industry expertise, their goals are naturally aligned. If a start-up is owned by its CEO, the CEO will determine its goal—which, in the cases I’ve researched, is to become a technology leader in the CEO’s industry of choice.

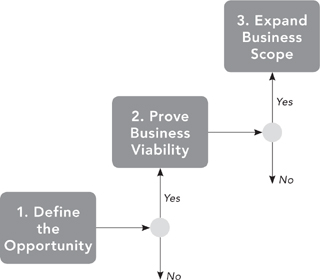

While each of the companies I interviewed applies this concept differently, there seems to be a common pattern they all share. As depicted in Figure 1.2, start-ups set goals according to the following sequence:

Real Option 1: Define the market opportunity. While it is somewhat amazing to me, some VCs are willing to give a management team millions of dollars to take a vague idea about a particular problem facing a group of customers and let them try to figure out whether they can develop a version of their idea that attracts customers fast. Determining whether enough customers will use the start-up’s prototype is the goal of the first real option.

FIGURE 1.2 Hungry Start-Up Approach to Short-Term Goals.

Real Option 2: Prove business viability. If the result of that first frugal experiment is positive, then the VC is likely to invest in another. The goal of the second investment is to try to sell the product resulting from the first experiment to enough customers to make a fact-based estimate of the likely size and potential profitability of the business. Deciding whether the business is viable is the goal of the second real option.

Real Option 3: Expand business scope. If the result of that second frugal experiment is positive, then the business may have generated as much as a few million dollars in sales. This is not a big enough business to interest potential buyers and therefore it sets the stage for the final goal. The goal of the third investment is to try to scale the business to the point where the founder can sell shares to the public, to an acquirer, or to capital providers willing to pay a higher price for its privately held shares.55 Getting the business to a size where investors can realize a return is the goal of the third real option.

Benefits of Real-Options Approach to Start-Up Goal Setting

There are three ways that start-ups benefit from the real-options approach to goal setting:

It bounds risk. The real-options approach to goal setting puts a clear limit on how much risk investors will take and it makes clear what kinds of returns that risk could generate. At a minimum, real options are almost guaranteed to generate information that can be useful for decision making. If that information leads to a decision to invest again, real options can boost the odds that investors—including the CEO and top managers who own equity in the firm—will achieve an attractive return on their investment of capital and effort.

It focuses the company. The real-options approach to goal setting helps to focus the efforts of a company’s relatively small employee base. It forces to the top of employees’ awareness that the money available to pay them will run out within a fairly short period of time. The CEO’s job here is to make it clear to all employees what they need to do in order to contribute to the company’s current goal. And that clear focus also boosts the odds that the company will succeed enough to persuade investors to grant it another round of capital.

It maps a growth path. Finally, the real-options approach to goal setting helps the organization keep in mind the bigger picture as it becomes focused on the start-up’s day-to-day activities. Particularly during the first real option stage, the start-up can motivate people more effectively if they have a map of the longer-term trajectory of the start-up if it achieves all the goals needed to reach the ultimate outcome.

HUNGRY-START-UP GOAL-SETTING TACTICS

How can a start-up CEO turn these general guidelines into useful action? This section provides tactical advice on how to pick a compelling mission, how to choose long-term goals, and how to set short-term goals.

Effective start-up missions share the following characteristics:

Important to the founder. Effective start-up missions are invariably extremely meaningful to their founder. That meaning springs most frequently from two sources, a strongly held belief that there is an untapped market opportunity and a personal passion that the founder believes he or she must pursue.

Relatable. A corollary to the first characteristic is that an effective startup mission is compelling not solely to the founder but also to other people that could help the start-up get off the ground. More specifically, missions that help a start-up hire talented people or get customers to try its product work best.

Spur value creation. Finally, a mission that spurs people to create a competitively superior product for its target customers helps a start-up prevail. An example of this is BrewDog—whose focus on creating high-quality beer that its founders and employees prefer helps it take share from so-called corporate beer purveyors.

Effective long-term goals are specific, measurable, and time-linked. And such long-term goals should be measured in ways that people in the company can understand. For example, people can more easily understand goals for getting a specific number of new customers than they can more abstract market-share target. Similarly, it helps in recruiting for a start-up CEO to make it clear that he sees the company going public in some specified time period or remaining independent.

How Start-Ups Define Useful Short-Term Goals

Real Option 1: Define the Market Opportunity

How long should a start-up take to determine whether it can develop a viable business model? The answer depends on how much capital the firm has and how much capital it needs to test the business model ideas. A start-up’s first real-option should make room for as many frugal experiments as it can execute given the rate at which it is burning through its scarce resources.

To know whether a venture has found a viable market opportunity, the entrepreneur must answer these four questions in the affirmative:

Does a basic version of your product attract a small initial group of users that’s passionate about your product?

Do those initial users keep using the product after the first try?

Do the users recommend the product to other people?

Do initial users get more value from the product by recommending it?

Use the following approach to get yes answers to these questions:

Listen to early adopter customers—the people who always like to be the first to try a new product—to uncover their unmet needs.

Build and give them a simple version of the product to get feedback.

If they like the initial version, ask them if they will recommend it to others.

If they don’t like it, find out what they don’t like about it and what’s missing, and try again.

Real Option 2: Prove Business Viability

If you can define the market opportunity, the next question is whether you can get people to pay for your product. If that effort is successful, then your business may be viable—particularly if the sales to those paying customers are greater than your costs.

One way to test a start-up’s viability is to consider a freemium strategy. By getting a fraction of 1 percent of those customers to pay for a more fully featured version of the product, companies can use the freemium strategy to become a viable business.

Jason Lemkin is VP of Web business services at Adobe and he explained that his start-up EchoSign was acquired by the maker of Flash in July 2011. Lemkin started EchoSign in January 2006 to help people get contracts signed and filed electronically.56

EchoSign offered a way to integrate contract signing with customer relationship management systems and it gave its product to customers at no charge—with the idea that they would pay for a premium version. When Adobe came looking for a big player in the electronic contracting space, it knocked on EchoSign’s door and bought the company.

In the four and a half months since that deal closed, Lemkin was thrilled to report that EchoSign’s integration with Adobe Reader had given him more new users than he had prior to the acquisition—and it then had a total of five million people using the product.

But here’s where the beauty of the freemium strategy comes in—even though a small fraction of those users were paying customers—that amounted to paying customers in the tens of thousands—including salespeople from Groupon and sales representatives from British Telecom.

By charging these more sophisticated users $100 a month for an advanced version of the product, EchoSign generated some pretty significant revenue from that small percent of users who paid—at that pay rate; EchoSign is a multimillion-dollar revenue business.

It hasn’t always been smooth sailing for Lemkin’s freemium strategy. Here are three lessons he’s learned:

It takes time. A company using a freemium strategy has to be patient and must make it extremely easy for users to sign up. In Lemkin’s experience, it can take three months for a start-up company that signs up to use EchoSign extensively, and another three to five months before that user feels compelled to buy the premium version of the product. This means that it takes a long time for the business to reach $10 million in sales, less time to double to $20 million, and after that it starts growing virally.

Invest to make the free version very compelling. Lemkin sees DropBox—a free service that lets users take their photos, documents, and videos anywhere and share them easily—as a compelling free utility that produces instant customer value. But if 20 percent of the users convert after, say, a month, then the service is not really freemium—it’s a free trial for a short period of time.

Need millions of free users. When Lemkin started EchoSign, he thought of eFax—then a $200 million service—as a good model of what his company could become. eFax had 10 million users and 10 percent of them paid. As it turned out, Lemkin was overly optimistic when he assumed that EchoSign would garner a similar 10 percent.

Nevertheless, with many of EchoSign’s current customers paying, Lemkin was happy with how its freemium strategy was working once it became part of Adobe.

EchoSign’s success with its freemium strategy illustrates the difference between finding a market opportunity and proving a start-up’s business model. When customers used the free version of Lemkin’s product, he proved to himself and his investors that he had found a market opportunity because people were using his product and recommending it to others.

However, it was not until EchoSign had gotten a critical mass of users and enough of them began to pay for the service that it began to generate sufficient revenues to become “cash-flow positive.”

Real Option 3: Expand Business Scope

Once a business has proved its viability in one market, the next short-term milestone is expanding it to other markets. The new markets could be in different countries or they could be a new group of customers within the company’s home market.

Here are some tests to decide whether the potential new market is likely to boost the start-up’s profitability:

Are the potential revenues and profits in the new market sufficient to offset the cost of serving it?

Does the start-up have the products and business capabilities needed to offer customers in the new market a competitively superior value proposition?

Are these competitive advantages enough for the start-up to gain a meaningful number of customers?

BrewDog’s expansion into twenty-seven countries is a case in point. Its first customers were in Sweden because an influential blogger liked its product and let his readers know. This helped BrewDog ink a contract with a leading Swedish beer distributor. And since such distributors relieve suppliers of the cost of operating a local operation, they can generate significant profits for the supplier if the product is in high demand. Most likely, Brew-Dog repeated this successful pattern to add twenty-six more countries to its collection of markets.

GOALS: DO YOU HAVE THE RIGHT ONES?

The foregoing discussion of goals may be raising questions in your mind about whether your start-up has the right ones. To help think about this question, here are some more detailed questions that may help you reach a conclusion:

Do you feel a connection between your passions or intellectual interests and your start-up’s long-term goals?

Have you considered whether pursuing those passions or intellectual interests will satisfy a widely shared human need?

If not, are you willing to take the risk that your start-up may not be able to generate sufficient revenues?

How confident are you that enough potential customers could benefit if your start-up achieves its long-term goal?

Have you developed a sequence of short-term goals that build on one another?

Do you have specific measures in mind that will help you determine objectively whether your start-up is on track to achieve the short-term goals?

Are you prepared with a back-up plan in case your start-up does not achieve its short-term goals?

If you have solid answers to these questions, then your long- and short-term goals have been set in a way that will serve your venture well. And if not, these questions may help you rethink your long- and short-term goals until you do have solid answers.

SUMMARY

People respond to goals—particularly if they can benefit from their achievement. In order to get a venture off the ground, entrepreneurs must provide them with an initial puff of inspiration. The goal is to create a hunger for creating a new world—or at least to create a start-up with a long-term goal that attracts talented people and ultimately customers and capital for growth. Whether that long-term goal springs from responding to market opportunity, solving personal pain, following the research, or a combination, it is critical that the mission be meaningful to the founders. And while a start-up’s long-term goal ought to remain constant, it is also important that entrepreneurs create a roadmap of sequential short-term goals the achievement of which will ultimately realize that long-term goal.

Why should I join your start-up? Mission. The mission is the entrepreneur’s most compelling case for why the start-up is going to achieve greatness. At the core of this case is a passionately held belief that what the start-up aspires to do is important. As we’ll see, that passion might come from the desire to make the world a better place, the excitement that comes from being certain that the start-up could capture a great economic opportunity that nobody else has seen, or the simple desire to solve a problem that perplexes the founder.

Why should I join your start-up? Mission. The mission is the entrepreneur’s most compelling case for why the start-up is going to achieve greatness. At the core of this case is a passionately held belief that what the start-up aspires to do is important. As we’ll see, that passion might come from the desire to make the world a better place, the excitement that comes from being certain that the start-up could capture a great economic opportunity that nobody else has seen, or the simple desire to solve a problem that perplexes the founder.